ThreeSixty Research Market Update April 2014

MARCH MARKET PERFORMANCE

The Pulse

|

|

The upward trend in advanced economy business surveys faltered toward the end of 2013 and this has continued into early 2014.

Nevertheless, this softer note probably reflects bad weather disrupting supply chains. There is no evidence in financial markets or forward looking business surveys, that the predicted gradual upward trend in global growth has been called into question.

Advanced economy growth has picked up, largely reflecting trends in industry and other sectors. Yet, service sector activity in the latter half of 2013 was held back by government shutdowns, fiscal austerity and consumer caution.

Emerging economy growth has flat-lined as expected and looks set to continue.

US

Across the Pacific, GDP growth is expected to decelerate modestly in the March quarter, partly reflecting the temporary impact of a severe winter. Quite a few economic indicators have weakened; however, it is not possible to quantify how much of this is weather related.

After a large fall in January, the manufacturing survey recovered some ground in February. But we saw the non-manufacturing indicator fall to its lowest level in four years – although it still remains above 50, which indicates continuing growth.

Not all partial indicators have weakened. Initial jobless claims have been relatively flat on a trend basis, business investment has held up, and even housing construction continued to grow through January.

On the monetary policy front, the current pace of Quantitative Easing tapering is likely to continue through to the end of Q4 2014. However, the Federal Reserve’s funds rate is likely to be on hold until well into 2015.

After a couple of soft months, non-agricultural employment grew by 175,000 in February, despite the severe weather conditions. The weak December and January readings were also revised up a little.

Europe

The Euro-zone grew by 0.3% in the December quarter, an annualised rate of around 1.2%. Growth was helped by rising exports and improving investment. However, over the 2013 year, GDP actually fell by 0.5%.

Retail sales in the Euro-zone rose by 1.6% in January, offsetting the previous month's 1.3% decline. A modest decline in the Purchasing Managers’ Index to 53.2 points was experienced in March, down from February’s 32-month high of 53.3 points. A value above 50 indicates economic expansion.

The economic recovery is not expected to be strong enough to make any real dent on unemployment this year; however, encouraging signs are emerging. The number of persons employed increased by 0.1% in the Euro-zone during Q4 2013.

European Union annual inflation was 0.8% in February 2014, down from 0.9% in January. Labour-market slack is expected to keep inflation low, though the Eurozone is expected to dodge outright deflation.

China

Premier Li Keqiang confirmed China’s growth target at “about 7.5%” for 2014, but noted that reform was the Government’s top priority. While the target is notionally unchanged from last year, comments by other government officials suggest that there could be some flexibility this year.

Growth in industrial production slowed significantly in February to 8.6% (well below market expectations of 9.5%), down from 9.6% in December 2013. This level is the lowest recorded since May 2009, when China was recovering from the global financial crisis. The downward trend in industrial production was unsurprising given the falls in manufacturing across recent months.

Trade data in February was particularly weak. This appeared to spook global markets, despite the fact that it followed unexpected strong levels in January. This volatility reflects the timing of Chinese New Year.

The Consumer Price Index has continued to slow from the recent peak in October 2013. In February, consumer prices increased by 2.0% - down from 2.5% when compared with January.

In early March, China recorded its first domestic corporate bond default. This has raised concerns regarding China’s shadow banking system.

Asia region

Over in India, the pace of their economic growth was 4.7% in Q4 2013, which was below market expectations and slightly slower than that recorded in the previous quarter. This outcome lines up with the poor performance shown in the monthly output and international trade data of late 2013, where there was no sign of rebound activity.

Across in East Asia, slow growth continued into early 2014 for exports and industrial output. Japan’s GDP for the December quarter has been revised downward to 0.7% annualised, due to a lower rise in capital investments and consumer spending. Japan's annual consumer inflation hit a five-year peak of 1.3% in January, although it remains well below the central bank's target of 2%.

Moderate economic growth continues across the emerging market economies of East Asia (ASEAN, Hong Kong, South Korea and Taiwan), with the pace of regional growth quickening from just under 4% in September to 4.3% in December 2013. The export-driven economies of Taiwan and South Korea accounted for most of the acceleration, as ASEAN growth was held down by political tensions in Thailand and financial/inflation issues in Indonesia.

Australia

Back home, the Australian economy grew 0.8% in the December quarter. This resulted in an annual GDP growth rate of 2.8%, which is below the rate needed to prevent rising unemployment.

Labour market indicators are mixed and suggest that an improvement in January may have been unwound in February. The unemployment rate rose to 6.0% in January and continues to be suppressed by weakness in the participation rate, currently 64.5%.

This pattern of jobless growth is set to continue as labour-intensive mining construction is replaced by capital-intensive mining production over the next few years. The NAB Consumer Anxiety Index rose to 61.7 points in March, compared with 61.5 points in December 2013. This was largely driven by heightened concerns over job security.

Private business investment continues to be the weakest area of domestic demand, declining by 3.4% in underlying terms in December 2014. There has been a sharp decline in new machinery and equipment investment (-8.2%), which is now 16.6% lower than a year ago.

Forward indicators signal little likelihood of an improvement in growth. The tentative improvement in NAB business conditions since late 2013 fell away in February driven by poorer conditions in manufacturing and wholesale (a bellwether industry), while forward orders weakened.

On a positive note, business confidence remains better than during much of last year, although it drifted down a little in February.

Equity markets

|

Australian Equities

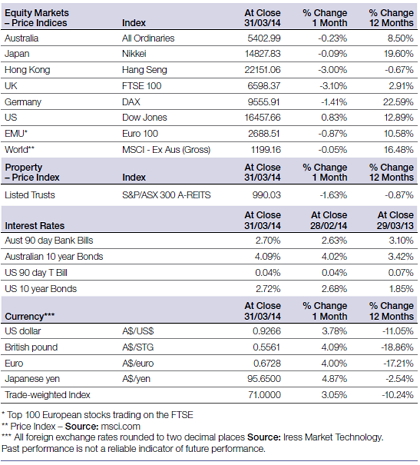

After a strong February and the conclusion of the reporting season, the Australian equity market experienced a relatively flat month in March. The S&P/ASX 300 Accumulation Index had a subdued month, increasing by only 0.21%, largely propped up by the banking sector.

However, the S&P/ASX All Ordinaries Index was down in March, posting a return of -0.23%, due to a fall in smaller cap stocks.

For the 12 months to 31 March 2014, the S&P/ASX 300 Accumulation Index posted a reasonable gain of 12.97%; while the large market caps, comprising of the S&P/ASX 50 Accumulation Index, performed even better, returning 14.50%.

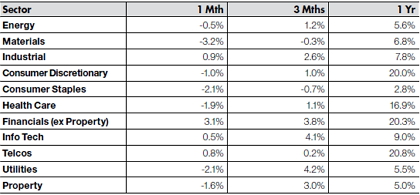

The best performing sectors in March were Financials, Industrials and Telecommunications. All three were solid performers, returning 3.1%, 0.9% and 0.8% respectively for the month.

The Materials, Consumer Staples and Utilities were the worst performing sectors in March, decreasing by -3.2%, -2.1% and -2.1% respectively.

Big movers this month

Going up: Financial (ex Property): +3.1%

Going down: Materials: -3.2%

Global equities

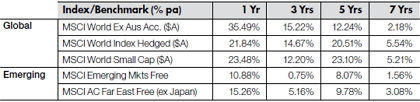

The MSCI World (ex-Australia) Accumulation Index was marginally down in March (-0.05%), after a strong rebound in February.

The US Dow Jones Index was up 0.83% in March – one of the few global markets to post solid returns in March.

The Nikkei, which had been a standout performer over the past 12 months, has been overtaken by Germany’s DAX. While both were down in March (-0.09% and -1.41% respectively), over 12 months returns have been quite strong (19.60% and 22.59% respectively).

Most other global markets were down in March, somewhat offsetting the broad market bounce experienced in February. The largest falls were felt in the UK (-3.10%) and Hong Kong (-3.00%).

Property

In March, the S&P/ASX 300 A-REIT Accumulation Index posted a -1.63% fall, once again underperforming the broader S&P/ASX 300 Accumulation Index.

On a 12 month rolling basis, property continues to underperform compared to the ASX 300 Accumulation Index. In fact, the 12 month return for the S&P/ASX 300 A-REIT Price Index is now negative for the year to March (-0.87%), compared to the All Ordinaries’ rise of 8.50% for the same period.

Over the long-term, global property has continued to outperform the Australian listed property sector. Global property, as represented by the UBS Global Investors Index was up 14.56% over the rolling one year period. However, the sector has a steep fall in March of -3.60%.

Fixed interest

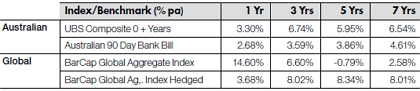

US 10-year bond yields inched higher in March, to close the month at 2.72% (up 0.04%). Australian 10-year bond yields were also up and closed the month at 4.09% (up 0.09%).

Australian bonds were relatively subdued during March. For the month, the UBS Composite Bond All Maturities Index posted a return of 0.02%.

Global bonds, as measured by the Barclays Capital Global Aggregate Index, were mixed against the Australian index. The unhedged index posted a fall of -3.51% for March, while the hedged equivalent had a positive return of 0.31%.

On a 12 month basis, Australian bonds returned 3.30%, but underperformed relative to unhedged global bonds that were up 14.60%. Hedged global bonds were also higher returning 3.68%.

Australian dollar

In March, the Australian Dollar (AUD) was up relative to most major currencies. The AUD increased 3.78% against the US Dollar (USD) to finish the month at 92.66 US cents. Over the past 12 months the AUD has declined significantly against the USD, down 11.05%.

The largest AUD rise in March was against the Japanese Yen (up 4.87%). On a 12 month basis, the AUD is down -2.54%.

Against the Euro, the AUD was relatively was up 4.00% during March, but is down 17.21% for the 12 month period. The largest 12 month fall in the AUD was relative to the British pound (down -18.86%).

The information contained in this Market Update is current as at 7/4/2014 and is prepared by GWM Adviser Services Limited ABN 96 002 071749 trading as ThreeSixty Research, registered office 150-153 Miller Street North Sydney NSW 2060. This company is a member of the National group of companies.

Any advice in this Market Update has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on any advice, consider whether it is appropriate to your objectives, financial situation and needs.

Past performance is not a reliable indicator of future performance.

Before acquiring a financial product, you should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product.