ThreeSixty Research Market Update February 2014

JANUARY MARKET PERFORMANCE

The Pulse

|

|

Global economies

The International Monetary Fund (IMF) has revised its 2014 global forecasts, with growth revised up to 3.7% from the October forecast of 3.6%. (NAB’s forecast is 3.5%). IMF has also forecast the following:

-

US growth revised to 2.8% from 2.6%

-

UK growth revised to 2.4% from 1.9% , and

-

China growth revised to 7.5% from 7.3%.

The IMF again urged advanced economies to maintain very accommodative monetary policy, due to the risk of deflation if there’s an adverse shock to economic activity.

The 2015 forecast remains at 3.9%.

US

The United States’ recent partial indicators of economic activity have generally been positive for the December quarter, with solid to strong readings for total consumption, business investment, and exports.

Moreover, inventory accumulation has been greater than expected so far during the quarter. As a result, NAB has revised its forecast for the December quarter to 0.7% (quarter on quarter; 3.0% annualised rate). While this would be a slower growth rate than in the September quarter, the result would indicate the US economy has strengthened at the end of 2013.

Annual average growth in 2014 is expected to be stronger than in 2013 as the headwind from fiscal policy is becoming more muted and fiscal policy uncertainty has fallen – although the debt ceiling remains a risk.

Europe

Over in Europe, the threat of deflation remains a risk with the Eurozone consumer price index increasing just 0.8% in December. This was lower than November’s 0.9% figure, while year on year the inflation rate fell to 1.3% in 2013 (about half of the 2012 rate).

If the Eurozone finds itself in a deflationary period the cost to governments servicing their debts will increase, making the task of debt reduction harder than it already is. As inflation falls, expectations are increasing that the European Central Bank (ECB) will be forced to take action.

In positive news for the region, the European economic recovery is gaining momentum after industrial production was up 1.8% in November (compared with a decrease of 0.8% in October), with car sales increasing three months in a row. In the past, confidence in the economy and car sales have been seen to move in tandem, as consumers are more willing to purchase cars when the economy’s long-term prospects are looking up.

In the UK, the inflation rate in December fell to the Bank of England’s 2% target for the first time in four years.

In Ireland, sentiment was lifted by a positive credit rating upgrade from Moody’s, a rating agency. According to Moody’s, the Irish economy has now recovered its growth potential after the Irish government exited its bailout program on schedule in January.

China

China’s latest National Accounts data shows that the economy grew by 1.8% quarter on quarter in December, and 7.7% year on year – representing a marginal slowdown from the September quarter.

For the full year, China’s economy expanded by 7.7% - the slowest rate of growth since 1999.

Despite intentions to rebalance the economy, the main contributor to China’s economic growth in 2013 was investment, followed by consumption.

Investment was further boosted mid-year by the mini-stimulus program, which largely focused on infrastructure spending. In contrast, net exports were modestly negative for economic growth, at -0.3 points - the weakest export contribution since Q3 2012.

The slowing trend for China’s economy is expected to continue into 2014, as the government becomes increasingly focused on its reform agenda.

Asia region

Japan’s growth is expected to slow from last year’s pace as the initial boost from ‘Abenomics’ wears off and reforms take effect. Even so, the Bank of Japan will seek to cushion the blow through extra monetary easing.

Interestingly, leading indicators pointed to solid growth in Q4: the manufacturing Purchasing Managers’ Index (PMI) reached its highest level in November since July 2006.

External trade has also improved over the past six months, partly reflecting the weakening of the Yen. However, business investment plans remain muted and wages have not adjusted to the new inflation environment.

The market’s consensus view for Japan’s GDP growth in 2014 stands at 1.6%, down from 1.9% in 2013.

Australia

Back at home, employment growth in the economy remains weak, reflecting the below trend growth in the economy and the ongoing softness in non-mining investment.

The December labour market figures were worse than expected, due to employment falling in every state except Western Australia. The overall result was well below NAB’s and the market’s forecast, however the unemployment rate remained unchanged at 5.8%.

These employment figures will keep the RBA on an easing bias and reduces speculation that the RBA is preparing to raise rates. NAB maintains the view that the unemployment rate will rise to over 6% in coming months.

Housing finance approval values rose 1.7% in November, the tenth increase in the past 11 months, despite the poor employment figures. Owner occupied approval values rose 1.9% and investor approvals rose 1.5%.

In trend terms, housing finance approvals are rising by approximately 2% per month – and are consistent with other housing indicators.

Low interest rates and rising house prices have clearly increased buyer interest. With interest rate rises unlikely in the short-term, housing finance approvals will continue to rise in 2014.

On balance, it’s likely that the RBA will keep interest rates on hold for at least the next few meetings. While the positive housing outlook and higher than expected Q4 inflation figures could give reason for an increase, this is being offset by generally soft economic figures and worsening employment.

Equity markets

|

Australian Equities

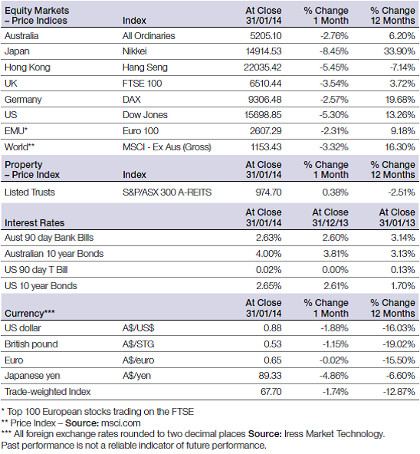

The Australian market started 2014 on a poor note. After a good year for Australian equities in 2013, the S&P/ASX 300 Accumulation Index lost ground, falling 3.00% in January.

The S&P/ASX All Ordinaries Index was also down in January, posting a return of -2.76%.

For the 12 months to 31 January 2014, the S&P/ASX 300 Accumulation Index posted a reasonable gain of 10.58%, while the large market caps, comprising the S&P/ASX 50 Accumulation Index, performed even better returning 12.85%.

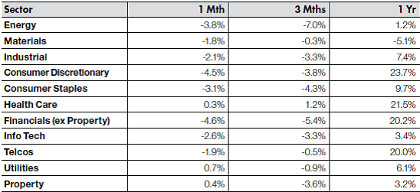

Surviving the January fall were the Utilities, Property and Health Care sectors. All three managed to stay in positive territory, returning 0.7%, 0.4% and 0.3% respectively for the month.

The Consumer Discretionary and Financials (ex-Property) were the worst performing sectors in January, both taking quite a hit, losing 4.5% and 4.6% respectively.

Big movers this month

Going up: Utilities 0.7%

Going down: Financials (ex-Property) -4.6%

Global equities

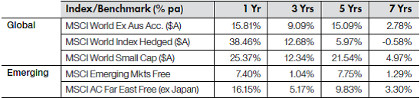

The MSCI World (ex-Australia) Accumulation Index was down 3.38% in January, which was a huge turnaround after the stellar returns of 2013.

The US Dow Jones was hit hard, posting a 5.3% loss in January. Markets have not taken the news of the U.S. Federal Reserve’s tapering program well.

Despite the falls that occurred during January, with the exceptions of Hong Kong’s Hang Seng Index and the UK’s FTSE, most of the major equity markets have posted solid 12 month returns.

The Nikkei has been a standout performer over the past 12 months, returning 33.90% to 31 January, even though it suffered the largest loss of the majors during January.

Property

In January, the S&P/ASX 300 A-REIT Accumulation Index posted a 0.41% return, bucking the trend of what was otherwise a predominantly negative month for investors.

On a 12 month rolling basis, property continues to underperform when compared to the ASX 300 Accumulation Index. The S&P/ASX 300 A-REIT Accumulation Index was up only 3.17% for the year to January, compared to the ASX 300 Accumulation Index which rose by 10.58% for the same period. Over the long-term, global property has outperformed the Australian listed property sector.

Fixed interest

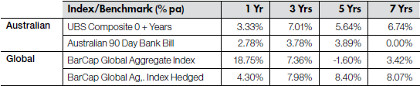

US 10-year bond yields inched higher in January, to close the month at 2.65%, up 0.04%. Australian 10-year bond yields closed the month at 4.0%.

Australian bonds performed well during January. This was not unexpected as investment grade bonds usually perform well during times of poor equity market performance. For the month, the UBS Composite Bond All Maturities Index posted a quite respectable return of 1.09%.

Global bonds, as measured by the Barclays Capital Global Aggregate Index, also saw a very good month. The unhedged index posted an exceptional 3.62% gain, while the hedged equivalent rose by 1.67%.

On a 12 month basis, Australian bonds returned 3.33%, but underperformed relative to unhedged global bonds that were up 18.75%. Hedged global bonds were also higher returning 4.30%.

Australian dollar

In January, the Australian Dollar (AUD) fell 1.88% against the US Dollar (USD) to finish the month at 87.53 US cents. Against the USD, the AUD has declined significantly, down 16.03% for the last 12 months. Having said this, the AUD has gained ground in early February to be trading at just over 89 US cents on February 5.

The AUD was also down 4.86% against the Japanese Yen. This means the AUD is now firmly in negative territory against the Yen over the last 12 months being down 6.6% for the year to close at ¥89.33.

Against the Euro, the AUD was fairly flat, down only 0.02% during January, but is down 15.5% for the 12 month period. The AUD finished the month at €0.6487.

The information contained in this Market Update is current as at 5/2/2014 and is prepared by GWM Adviser Services Limited ABN 96 002 071749 trading as ThreeSixty Research, registered office 150-153 Miller Street North Sydney NSW 2060. This company is a member of the National group of companies.

Any advice in this Market Update has been prepared without taking account of your objectives, financial situation or needs. Because of this you should, before acting on any advice, consider whether it is appropriate to your objectives, financial situation and needs.

Past performance is not a reliable indicator of future performance.

Before acquiring a financial product, you should obtain a Product Disclosure Statement (PDS) relating to that product and consider the contents of the PDS before making a decision about whether to acquire the product.